With the permission of Mr Tapiwa Dalu, the economist at Grant Thornton, the reputable tax advisers, we have put up on our website an article written by him which is an excellent explanation of the economic impact of the intermediated financial transactions tax (the tax imposed by the Government on RTGS transactions and other such electronic money transfers).

Summary of what the Analysis Covers

The Government recently increased the intermediated financial transactions tax from USD 0.05 per transaction to USD 0.02 for every dollar transacted. The Grant Thornton article analyses the impact of the new financial transaction tax on consumption (that is, demand and supply). The analysis covers:

- What Statutory Instrument 205 of 2018 states. This was also dealt with in our Bill Watch 32/2018 of 23rd October.

- Exemptions from the tax: These are all listed in the analysis.

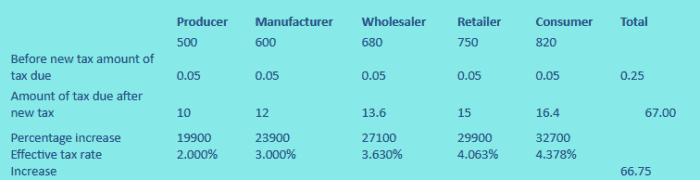

- Impact of the intermediated financial transactions tax – All stakeholders in the supply chain are affected by the tax, that is to say each supplier must pay the tax on every electronic money transfer he or she carries out. The tax increases the suppliers’ costs, and suppliers along the supply chain will want to cushion themselves against the increased costs of production and administration by passing on the tax to the final consumers so as maintain their profits. The effect of all these individual increases along the supply chain is to increase total costs exponentially. The percentage increase on the rate of tax would be 32 700% on the final consumer as depicted by the table below [based goods initially worth $500]:

Some of the effects of the tax, as outlined in the Grant Thornton analysis, are as follows:

- Increase cash transactions – the introduction of the intermediated financial transactions tax has the impact of reversing all the Government’s efforts pushing for a cashless economy and financial inclusion, as traders will try to be paid in cash in order to avoid paying the 2% tax

- Increase in the informal sector – as most taxpayers try to avoid paying the tax, they will move over to the informal sector and transact in cash

- Decrease in deposits – most traders and businesspeople will prefer to keep their hard-earned currency in cash and use it to purchase raw materials/ goods rather than have it deposited in a bank where they will incur tax whenever they want to effect a transaction or payment.

- Loss of competitive advantage – due to the increase in the cost of production and the prices of goods resulting from the 2% tax, Zimbabwean products may fail to compete on the international market.

- Double taxation – the 2% tax has an impact of imposing tax on tax. For example, when one is paying for raw materials or goods which are subject to Value Added Tax (VAT), the 2% tax is calculated on the amount inclusive of VAT. The 2% tax basically ignores all the rules on double taxation and taxes the consumer, trader, manufacturer etc. on VAT.

- Deductability of the intermediated financial transactions tax – section 16(1)(d) of the Income Tax Act prohibits claiming tax as an expense for income tax purposes. However, the intermediated financial transactions tax is in fact a cost/expense to the trader rather than a tax. The question is, will taxpayers be allowed to claim it as a deduction? The legislation is silent on this.

- Tax should be charged on revenue rather than on an expense – the 2% tax is basically taxing taxpayers on an expense and not on revenue. Again this is against the principles of taxation.

- Difficulty in tax calculation and collectability – Collecting agents (banks and financial institutions) will not know whether or not transactions are exempt from the tax unless the taxpayers come forward to explain the reason for their transactions. Hence we will have a situation where people are taxed on exempt amounts.

- Taxation of social basics – Also the tax ignores the income tax exemptions of goods/services, that is, the exemptions granted to payments of school fees, benefit funds and medical services/supplies. These goods and services have always been exempted from tax – income tax and VAT are also not charged on them.

- Increase in costs for the collecting agents – More people will have to be employed and systems will have to be upgraded in order to cope with the new tax system as it is basically being withheld on all transactions.

- Cost of production – The introduction of an indirect tax (intermediary financial transactions tax) increases the traders’ costs of production. This will increase the prices paid by consumers and decrease the sales/revenues of the sellers. The end result is that no matter who is taxed, the revenues that sellers receive will decrease and the prices consumers pay will increase; leading to a loss of welfare within the economy as consumers and producers are worse off than before the tax was introduced.

Source: Veritas